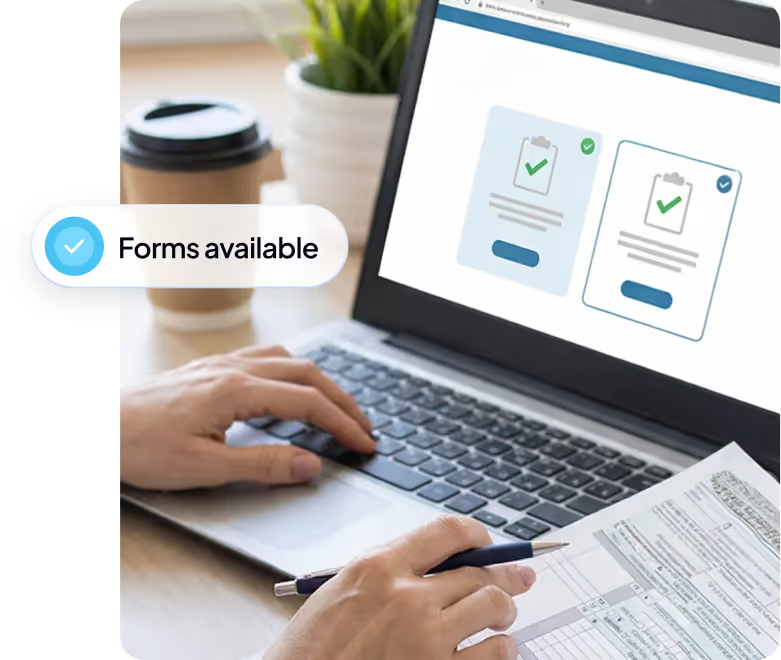

Know who you paid? We’ll handle the rest.

Whether someone is an employee or a contractor determines which form you need to file. We’ll remove the guesswork by clearly explaining the difference and guiding you to the right form for your needs.

Use a W-2 for employees

Employees work under your direction. You control how, when, and where the work is done, and taxes are withheld from their pay.

Common examples:

Full-time or part-time staff

Employees on payroll

Workers receiving regular wages

Use a 1099-NEC for contractors

Contractors work independently. You pay them for services, and they handle their own taxes.

Common examples:

Freelancers

Consultants

Independent contractors

If you paid a contractor $600 or more, you are generally required to file a 1099-NEC.

Use a 1099-MISC for miscellaneous payments

This form reports specific types of income that aren’t reported on a 1099-NEC.

Common examples:

Rent payments

Prizes and awards

Royalties

Payments to attorneys

Other qualifying income over $600

If you made payments in these categories, you’ll need to file a 1099-MISC.

How It Works

Step 1 - Create

Choose your form type (W-2, 1099-NEC or 1099-MISC) and enter your payer and recipient details.

Step 2 - Submit

Review everything and securely e-file to the IRS and your state, when required.

Step 3 - Share

Send forms by email, print them yourself, or have Adams mail them for you.

Everything you need, where you need it

Whether you’re filing for employees, contractors, or both, Adams keeps everything organized and easy to manage.

File with confidence:

Accurate income reporting

Clear guidance on which form to file

Avoid IRS penalties

Built-in checks to catch common errors

IRS-compliant and always current

Flexible delivery options